Growth Strategies of Smaller Maritime Operators

HMM and Hanjin Shipping

The two largest maritime operators in

South Korea, Hanjin Shipping and HMM – Hyundai Merchant Marine, faced severe

financial difficulties, culminating in the bankruptcy of Hanjin Shipping in

2017. This marked the largest bankruptcy in the history of the container

shipping industry.

Both companies followed ambitious fleet

expansion strategies, resulting in unsustainable debt burdens in a market then

undergoing a generalized crisis. After a financial recovery plan was rejected

by the main creditors, Hanjin Shipping declared bankruptcy in September 2016.

This led to widespread supply chain disruptions, particularly affecting South

Korea's exports to the USA.

During the period leading up to

Thanksgiving and the festive season of Christmas and New Year in the USA, major

South Korean exporters like Samsung and LG, as well as Nike, saw their products

stranded aboard Hanjin's ships, which could not dock as they would be

immediately seized due to outstanding debts. On February 17, 2017, South Korean

courts declared Hanjin Shipping's definitive bankruptcy.

Interestingly, the sale of Hanjin's

assets, which amounted to 220 million USD, only covered 2% of the total debt

owed to creditors, which was 10.5 billion USD. The legal figure of credit

privileges (prioritizing the distribution of the value of the liquidated

assets), typically characteristic of shipping, only accentuated the precarious

negotiating position of the creditors.

In parallel, HMM – Hyundai Merchant

Marine, in order to address its liabilities, decided to divest its LNG

business. Its fleet of 10 LNG ships and associated operating contracts were

sold for 1.03 billion USD.

The intervention of the South Korean

government allowed HMM to remain operational during this difficult period,

which immediately led to criticism of its inaction during the bankruptcy of

Hanjin Shipping. Given the dramatic logistical impacts of Hanjin's bankruptcy

and the damage to South Korea's economic image, the South Korean government had

no alternative but to ensure the sustainability of HMM.

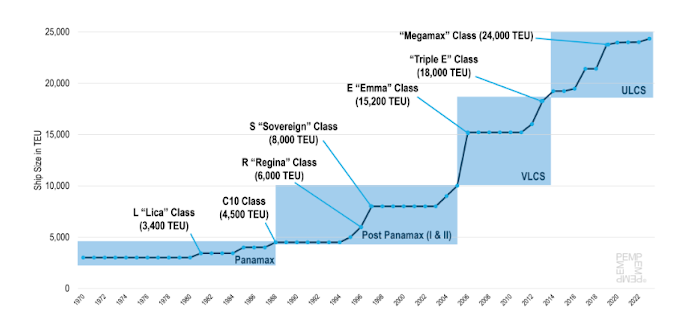

Currently, HMM is the 8th largest

container shipping operator with an order book of 265,000 TEU (33.8% of its

fleet). Interestingly, two of the world's largest ships, "HMM

Algeciras" and "HMM Copenhagen," with a capacity of 23,964 TEU,

are owned by HMM.

A reprivatization process is underway,

which once again did not achieve the desired effects. The acquisition offer

from Hapag-Lloyd (Germany) was not accepted for strategic reasons. In 2023, the

Harim Group submitted the winning bid (4.9 billion USD). Difficulties in

accessing bank credit also led to the failure of this operation. Currently,

with the market on the rise, the South Korean government is evaluating the best

strategic option to follow.

Main Maritime Shipping Operators

Source: Adapted by the author based on data from BRS ALPHALINER, Fleet Statistics (January 1, 2024)

Yang Ming / ZIM/ Wan Hai/ PIL

Yang Ming is the second-largest

container shipping operator based in Taiwan (9th globally), with an available

cargo capacity of 707,500 TEU. Its order book is the smallest among the top 20

global maritime operators, consisting of only five ships (mostly 14,000 and

16,000 TEU, representing 77,500 TEU).

ZIM, an Israeli maritime operator,

exemplifies a company that has followed an audacious growth strategy. It is

likely that by 2024, it will surpass Yang Ming, becoming the 9th largest

container shipping operator. Its fleet more than doubled between 2020 and 2024.

As of January 2024, ZIM has a fleet of

619,500 TEU and 29 ships on order at shipyards, representing an additional

cargo capacity of 222,000 TEU. It is also one of the few maritime operators not

part of any Strategic Alliance. It is expected to cooperate more actively with

MSC (after the end of 2M) but has no formal Alliance agreement.

Amid the proliferation of conflict in

the Middle East (Israeli-Palestinian conflict), the strategic importance of ZIM

to the State of Israel, which cannot rely on market contingencies for the

regular and continuous supply of the country, underscores ZIM's economic

significance. The Israeli state, through the "Golden Share" held by

the Israel Corporation (owned by the Ofer family), guarantees ZIM's continuity

and growth.

Wan Hai Lines, a Taiwanese maritime

operator founded in 1965, specializes in feeder traffic on the Intra-Asian

Route, one of the fastest-growing markets for container shipping. It has a

fleet of 120 ships, representing a cargo capacity of 483,000 TEU as of January

2024. Recently, Wan Hai Lines ordered a series of larger ships (13,000 TEU) and

aims to enter the East/West routes, already providing services on the

Transpacific Route (United States and Canada), South America, and trades with

Africa and the Middle East.

PIL, a Singaporean maritime operator,

has 12 new ships on order at shipyards. These represent a cargo capacity of

119,000 TEU, approximately 40% of its current fleet capacity (295,000 TEU).

The company follows a strategy focused

on the Intra-Asian market, complementing, in some ways, the global strategy of

the Evergreen Group (both owned by the YF Chang family). The economic capacity

of its shareholder ensures the company's sustainability for the future.

FERNANDO CRUZ GONÇALVES

Professor da ENIDH

0 Comentários